Protocol Insights #2

In this weeks coverage we look at popular liquid staking protocols and the recent activity around $ETC.

ETH 2.0 Liquid Staking - Overview

The overall staked supply of Ethereum stands at 11% or 13,142,680 $ETH tokens as of August 2022. The percentage of staked $ETH has grown significantly (47%) YTD as the merge narrative becomes clearer

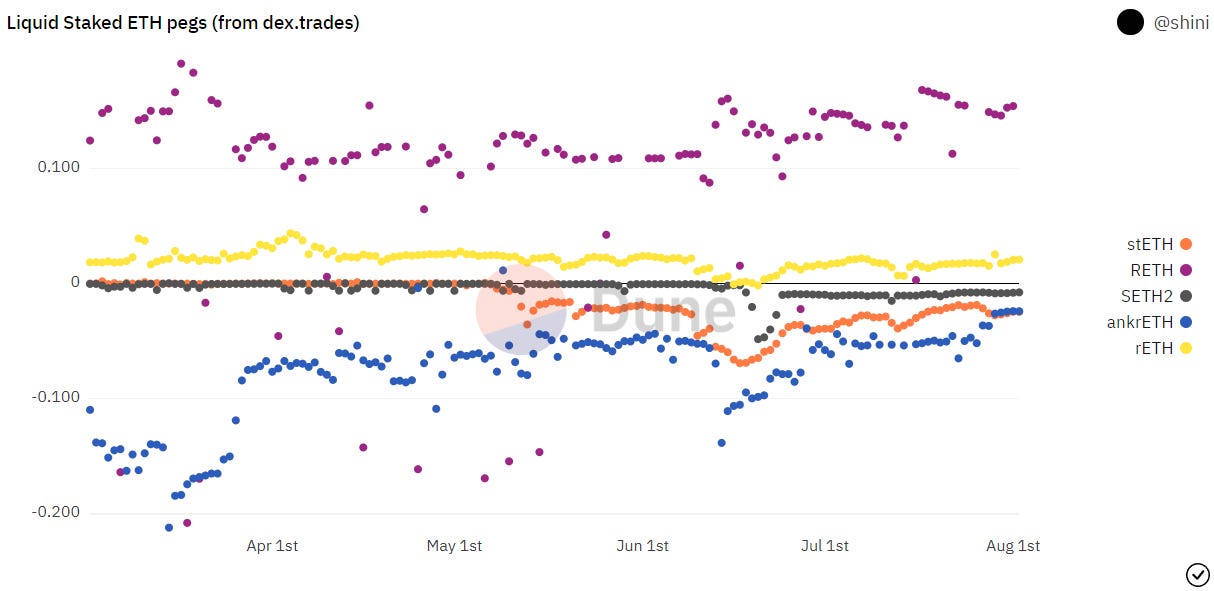

Liquid staking however has not been without its problems, tokens such as $stETH (Lido), $rETH (Rocketpool), $SETH2 (stakewise) recently faced depeg events to $ETH. Mainly as Celsius was forced to liquidate its $stETH position in the $stETH-$ETH Crv pool, which did not have sufficient liquidity to avoid impairment

Each pair fared differently, with $stETH peg trading as low as -7%, compared to $rETH which only traded at a discount briefly at just -0.065%. This was mainly because $rETH yield accrues to the same token while $stETH rewards are distributed via rebase

Source: @Shini The very recent depeg events of many liquid staked derivatives, coupled with the broader merge narrative may explain the dynamic shift from decentralized LSDs to centralized, non-liquid, stakers (e.g., Coinbase, Kraken etc)

Shares of staked $ETH during the last 7 days differs a lot from total shares, suggesting some shift in staking dynamics. Between July 25th to 1st August, we see:

Decentralized stake pools (Lido + Rocketpool) only saw 12.6% of staked ETH

Centralized staking pools (Coinbase, Kraken, OKEX) saw 53.2%

Others (Abyss, Batch deposit, Stakefish and some unknown addresses took 34.2%)

CHART showing centralised vs decentralised mix before and after //unable to find this chart, my recommendation is to let this point stay without a chart//

Price Action

July saw relief in PA across most of the market. Most DeFi and large cap alts saw 80-100% gains. Liquid staking protocols performed much better than the rest of the market boasting as much as 300-400% gains. This was largely driven by the narrative around merge, as the upgrade will likely be greatly beneficial for these protocols

Rocketpool token $RPL was also supported by the growing demand for Rocket nodes that require operators to buy and stake the native token

//charts can be displayed side-to side on final email//

① LIDO $LDO

Lido market share continues to stall, while recent $ETH stakers look to favor centralized pools and Lido DAO proposes to diversify treasury

Website | Discord | Dashboard

Lido continues to maintain the largest staked $ETH pools with 31.46% of the total staked $ETH supply. However, its market share has reduced slightly from 32.4% to 31.4% between May and August 2022. Along with this we see that the overall Liquid staking market share and supply has stalled since the May crash

Source: @LidoAnalytics We also noticed that between February and May 2022, Lido $ETH inflows were bigger than all other inflows combined. This trend saw a sharp change after $stETH depegged briefly in June. In July 22, Lido inflows were only 7.4% of overall inflow. Suggesting lesser confidence from investors towards ‘LSD’ pools

$stETH is the most widely used liquid ETH token in DeFi. Infact a majority of its supply is in the AAVE and Curve pools. This is a core reason behind Lido’s growing network effects and market share

Lido continues to hold over 80% of its treasury in its native governance token $LDO, posing significant concentration risk. A proposal to sell 1% of LDO supply to Dragonfly is currently under discussion, after a proposal to sell 2% for nearly 30 mn $DAI was rejected by the DAO. Most recently Lido raised $70 mn from a16z in March 2022, in total Lido has raised over $140 mn in private funding. The proposal seems to be for the purpose of diversification rather than securing runway for operations

Till August 2022, Lido has generated $32 mn in protocol fees, which comes from a 10% cut on the staking APR. The fee is split 50-50 between Lido DAO and node operators

② ROCKETPOOL $RPL

Rocketpool deposits grow despite slowdown in overall deposits to ETH2.0, staked $RPL supply continues to grow, reaching 34% in August

Website | Discord | Dashboard

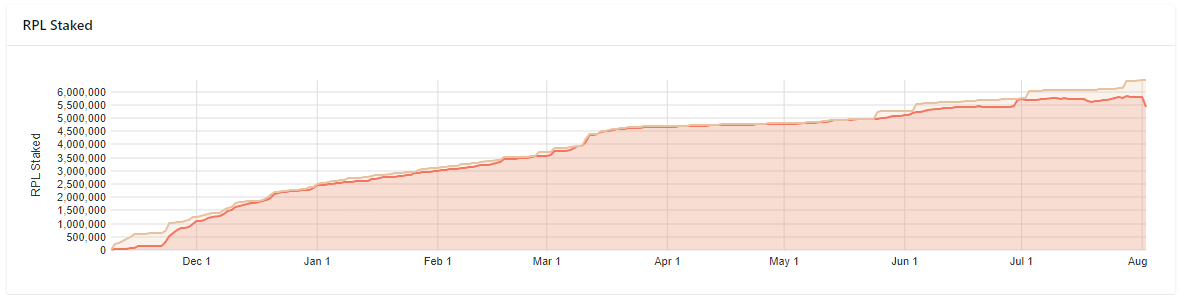

Rocketpool is the only decentralized staking pool that saw significant deposit growth between May and August. Deposits grew from 185,270 $ETH to 231,289 $ETH, a 24.8% increase in the same period. The number of nodes also grew from 0 to 1349 in 9 months of the protocol’s launch

Rocketpool’s native token is required as collateral for node operators to setup new nodes. The number of staked $RPL continues to grow steadily, currently over 34% of the supply is staked. The impact of the increasing staked $RPL supply can also be seen on the up-trending price of the token

The Rocketpool network is heavily depended on multiple but smaller node operators, who are also heavily long its native token $RPL. This poses severe growth challenges because even as the $ETH TVL grows, the network cannot add nodes at the same rate. At present only 203,760 $ETH out of its 231,492 $ETH is actually staked to the beacon chain

Rocketpool charges fees on unstaking, and in-general hovers between 10-15% for different nodes. Node operators can set their own fee if they satisfy the collateral conditions

What happens to Liquid staking solutions post merge?

The dangers of ‘LSD’, despite Lido’s dominance as the biggest staked pool, the consensus model for Ethereum is currently based on network hashing power. However once we are past the merge ‘Liquid Staking Derivatives’ or LSD pools will pose significant centralization risk for Ethereum unless their governance is sufficiently decentralized

Derivatives are the future, it is possible that the network effects of growing liquid derivatives supply could result in $ETH to become the currency mainly used for staking while LSD tokens become the primary token for DeFi and speculation. This is possible if the merge triggers more holders to stake their $ETH since the uncertainty around unstaking is gone

The MEV Opportunity, big pools like Lido will likely have natural monopoly over MEV opportunities on the new PoS chain, adding to value capture for their native tokens

Overall the merge will likely make Liquid staking pools more viable for new users as the terms become more predictable

3. Ethereum Classic $ETC

With the recent confirmation of the merge coming by September, many miners of the Ethereum network have started to look at alternative ways to utilize their equipment. This led to a revival of sorts for $ETC as miners look to bet on a new ecosystem on the PoW chain. $ETC jumped 3x from its June lows of 12.47 $USDT

At present in the Chinese miner community,

@BITMAINtech supports ETC 2

@ChandlerGuo leads the discussion on forking POW ETH

@BixinWallet expressed support for other POWs such as kadena, starcoin, aleo, ckb and conflux.

$ETC reached its ATH hashrate of 27.5 TH/s, this came in after some large miners such as Antpool publicly announced that they will be investing $10 mn as a start to support the growth of $ETC ecosystem. Additionally, due to the demand from their customers, Innosilicon released an updated firmware that adds $ETC support to their A10pro server products

Active address count on Ethereum Classic nearly doubled towards the end of July from 20k daily to 40k. While $ETC interest has surged, it is to be noted that a fork of the most recent pre-merge $ETH chain (ETHPoW) will likely be a stronger contender for miners and PoW proponents to shift to, as this version has more contracts and infrastructure.

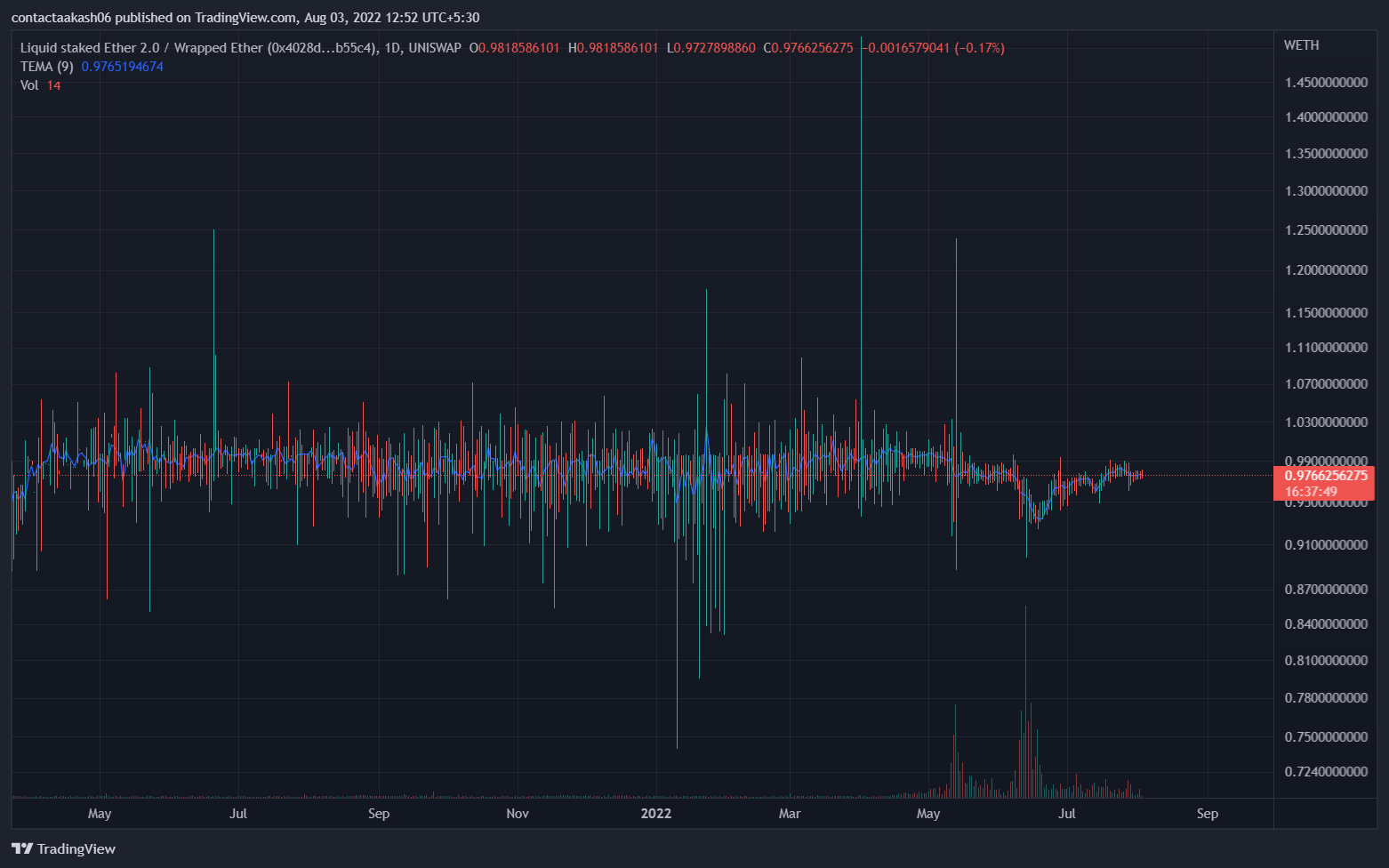

Another interesting metric that serves as an indicator for the value of a post merge PoW fork is the spread between $stETH and $ETH. Since $stETH can’t be redeemed for anything but ETH2, a higher expected value of ETHPoW would mean a greater $stETH-$ETH spread. As of 3rd August the spread is at 2.4%

At present prices and network activity the daily revenue pool for $ETH rewards stands at $22.8 mn. The daily reward pool for all the other major PoW chains including $ETC about $775,000. So unless the network activity and token prices grow massively, switching to these alt-chain will not be viable for miners